Institutional capital from pension funds to sovereign wealth investors is flowing into European mining at a pace not seen in decades. The message from Brussels is unambiguous: Europe must mine its own critical resources, and it must start now. Europe's Tech Future Cannot Be Outsourced!

At the centre of this transformation sits Sweden, ranked in the top 10 globally by the Fraser Institute for mining investment attractiveness, and one of only two European jurisdictions to earn that distinction.

Sweden accounts for 91% of Europe’s iron ore production, leads the continent in mineral output, and hosts geological formations that rank alongside the Canadian Shield and South African craton for mineral prospectivity.

For European investors seeking exposure to some of Europe’s most precious metals that will power the future of technology and AI. Sweden represents the premier jurisdiction on the continent.

At the Wall Street Investor Report, we focus on emerging companies that show strong potential within Europe's evolving resource landscape, and one Swedish mining company has continued to catch our attention closely: Svea Mining AB (Spotlight: SVEA | Frankfurt: SVEA), which stands out as one of the most compelling names in the European technology metals sector

With two copper-silver polymetallic system projects covering approximately 7,500 hectares in the world-class Skellefteå mining district of northern Sweden, Svea Mining aligns closely with the type of strategic European assets that institutional investors and EU policymakers are watching for.

Svea Mining's flagship Kalvträsk property sits on the margin of the Skellefteå mining district, within a setting that opens the door to copper-silver mineralisation consistent with the broader district's known assemblage, the same metal pairing that has long underpinned Europe's electrification and technology supply chains.

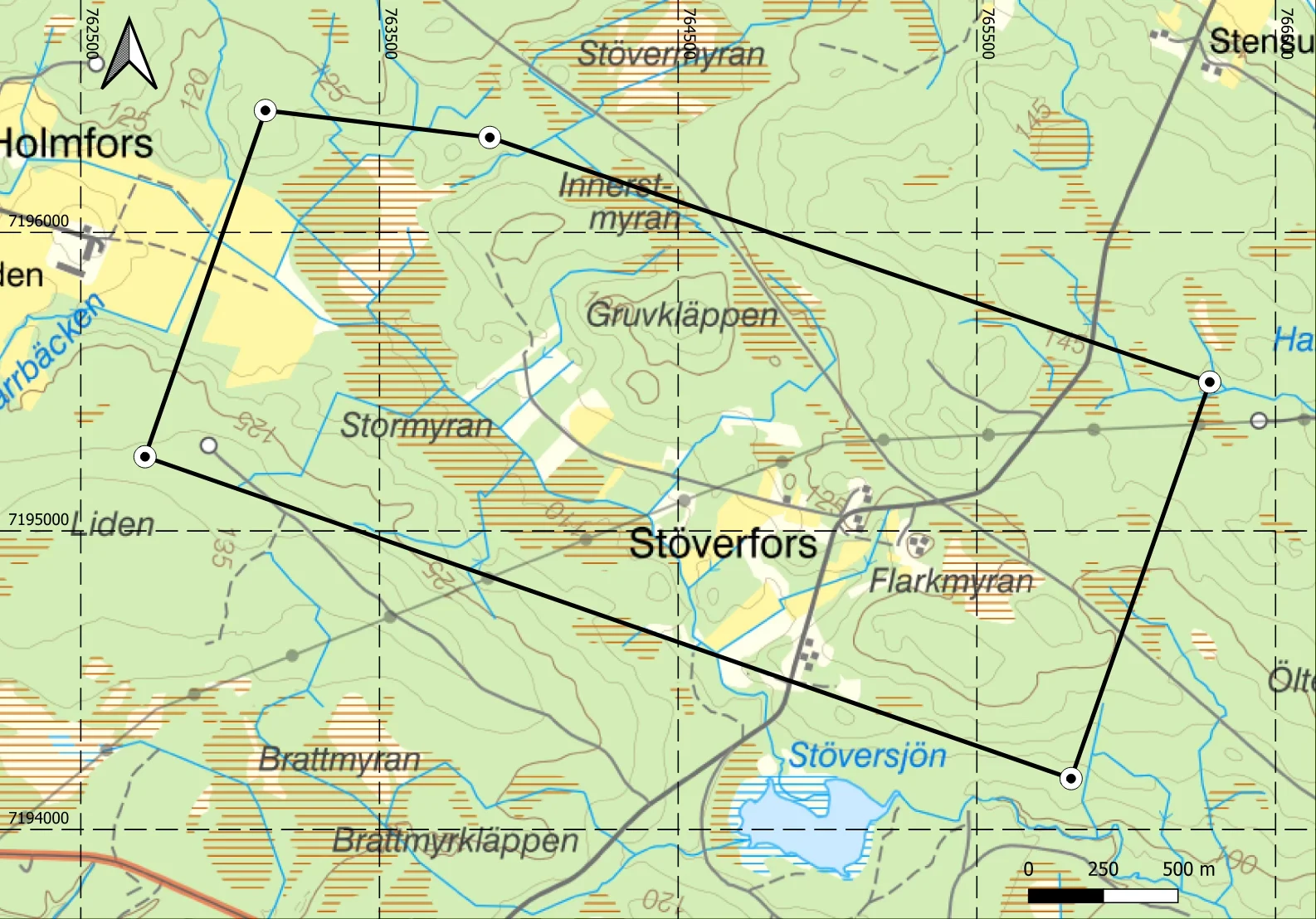

The company's Stöverfors project, accessible via local roads, sits within the Skellefteå VMS belt itself, a setting classically associated with copper-silver polymetallic systems, and benefits from a district that has supported continuous mining operations since the 1920s with well-developed existing infrastructure.

SGAB report BRAP 82108 identifies known bedrock outcrops and mineralised structures in the Stöverfors area within the same volcanogenic massive sulphide system that has produced copper, silver, and associated base metals across the district for over a century.

The transatlantic relationship that Europe relied on for decades is undergoing a fundamental shift.

The current U.S. administration has repeatedly cast doubt on its commitment to NATO's Article 5 mutual defense clause, threatened tariffs against longstanding European allies, and pursued the acquisition of Greenland, prompting Denmark's military intelligence service to label the United States a potential security concern for the first time in history.

The Pentagon's 2026 National Defense Strategy makes it explicit: European allies are now expected to assume primary responsibility for their own conventional defense, with only "critical but more limited" U.S. support.

In response, EU leaders convened an emergency summit in February 2026 focused squarely on reducing the bloc's vulnerability to external economic coercion from both the United States and China, with European Council President António Costa outlining five strategic pillars to strengthen the EU's economic autonomy.

At the heart of this shift is resource sovereignty. The EU still sources all of its heavy rare earth elements from China, and the bloc has committed €3 billion through its RESourceEU Action Plan to accelerate domestic extraction, processing, and recycling of critical raw materials.

The Critical Raw Materials Act now mandates that the EU source at least 10% of its strategic minerals domestically by 2030, and Sweden, which hosts the vast majority of the minerals on the EU's critical list, sits at the centre of that ambition.

This is where companies like Svea Mining come in, answering the push to explore for critical minerals like copper and silver, and committing as a European-based company to discovery that contributes directly to securing Europe's resource independence.

For Europeans investors, the message is increasingly clear: supporting homegrown mining projects is no longer just a financial opportunity, it is a strategic necessity and patriotic duty.

Companies like Svea Mining AB (Spotlight: SVEA | Frankfurt: SVEA), operating in one of Europe's most prolific mining districts and exploring for the copper and silver that underpin AI infrastructure and modern defence systems alike, stand to benefit directly from this generational shift toward continental self-reliance.

Copper is the industrial backbone of the modern economy, often called "Dr. Copper" for its role as a barometer of economic health, and its importance is accelerating across electrification, renewable energy, electric vehicles, grid infrastructure, and now the AI revolution reshaping global capital expenditure.

S&P Global's landmark study, Copper in the Age of AI, projects global copper demand will rise from 18 million metric tonnes in 2025 to 23 million metric tonnes by 2040, with a projected supply deficit of 10 million metric tonnes, a gap the study characterises as a "systemic risk for global industries, technological advancement, and economic growth."

Goldman Sachs estimates AI will drive a 165% increase in data centre power demand by 2030, with data centres alone potentially consuming more than half a million metric tonnes of copper annually by that point.

At the same time, Europe is undertaking its largest military rebuild since the Cold War, and that rebuild runs on copper. NATO members have committed to defence spending targets rising toward 5% of GDP, Germany has established a special fund worth hundreds of billions of euros to modernise its armed forces, and the EU's ReArm Europe plan aims to mobilise as much as €800 billion for the bloc's defence-industrial base.

Where past conflicts were won on steel, today's wars are fought on technology, and that technology runs on copper, the wiring, sensors, communications, and guidance systems behind every fighter jet, naval vessel, missile, and drone now demand more copper than steel ever required.

This defence demand is arriving on top of an already strained copper market, with the green transition, the AI revolution, and Europe's arms build-up all competing for the same metal.

China currently controls the majority of global copper refining capacity, making supply chain diversification an urgent strategic priority, and the EU's Critical Raw Materials Act explicitly names copper among its priority metals, with the RESourceEU Action Plan directing €3 billion in significant part toward securing European copper supply.

Europe can no longer afford to be at the mercy of others for the materials that power its economy and defend its borders, and this is precisely where companies like Svea Mining have a role to play. Svea Mining's commitment to its exploration properties in one of Sweden's richest mining jurisdictions reflects the kind of European grit this moment demands, positioning the company at the centre of the shift toward copper as the foundation of Europe's technology, AI, and defence future.

This is why we at the Wall Street Investor Report are genuinely excited about Svea Mining, a company we believe has assembled one of the most capable teams in European mining, with projects situated in one of the richest mining regions in a country known for its stability and strong governance.

Silver's reputation as a precious metal often overshadows its role as one of the most strategically important industrial metals in the modern economy, and for Europe's technology and defence ambitions, that role is becoming impossible to ignore.

Silver is the most electrically and thermally conductive metal known, properties that make it irreplaceable in the high-performance electronics now at the centre of AI infrastructure, advanced defence systems, and next-generation energy networks, and it is precisely this metal that Svea Mining is exploring for across its Skellefteå properties, alongside copper, in a classic copper-silver polymetallic setting.

In AI and data centres, silver is used throughout the circuitry, switches, and connectors that handle the enormous power loads of modern computing hardware, where even marginal gains in conductivity translate into real efficiency at scale.

Growth in photovoltaic technology, EVs, and AI data centres could widen the silver deficit, drive up prices, and attract fresh investor interest, with electric vehicles, 5G infrastructure, semiconductors, and medical devices all relying on silver's unique conductive properties. This is the demand backdrop against which Svea Mining's copper-silver exploration thesis is positioned.

In the defence industry, silver's role is just as critical, used in guidance systems, communications equipment, radar, and the high-reliability electrical contacts found in virtually every advanced military platform, applications where failure is not an option and substitution is rarely possible.

Svea Mining's properties sit within a geological system capable of hosting exactly this combination of metals, copper and silver together, the same pairing now being called on to supply both Europe's AI infrastructure and its defence rebuild.

The supply picture only sharpens the urgency. The Silver Institute has now tracked six consecutive years of global silver supply deficits. What makes the current moment particularly compelling is that silver pulled back sharply from its all-time high of $121.64 per ounce in January 2026 to trade near $67-69 as of June 2026 and through that entire drawdown, not one major bank cut its year-end price target. Most strikingly, Deutsche Bank, one of Europe's most influential financial institutions, is targeting $100 per ounce by the end of 2026 a figure that would represent approximately 45% upside from current levels. When institutions raise forecasts as a price falls, it signals conviction in the underlying thesis rather than momentum chasing and for silver, that thesis rests on a structural supply deficit that no short-term price correction can resolve.

As Warren Buffett famously said, 'Price is what you pay, value is what you get.'

With silver trading 40% below its all-time high while every major bank has raised its price target, the value has rarely looked stronger.

For a continent racing to secure the inputs behind its AI infrastructure and its defence rebuild, a domestically sourced supply of silver is not a luxury, it is a component of European security itself, and Svea Mining's exploration programme, targeting a copper-silver polymetallic system in one of Europe's most storied mining districts, is aimed squarely at helping close that gap.

Svea Mining is not just a copper, silver exploration company. Beyond exploring its own projects, the company intends to take strategic positions alongside established European producers and near term producers, with a particular focus on critical minerals that are central to the EU's resource sovereignty agenda.

Europe is home to some of the most significant mineral discoveries made anywhere in the world in recent years. Norway's Fen Carbonatite Complex, operated by Rare Earths Norway, now hosts an estimated 15.9 million tonnes of rare earth oxides, making it the largest deposit on the European continent. In Sweden, state owned LKAB has identified over 2.2 million tonnes of rare earth oxides at its Per Geijer deposit near Kiruna.

These are transformational Scandinavian resources, yet both are held by private and government-owned entities that offer no public market access. Everyday investors simply cannot participate in these opportunities directly.

This is where Svea Mining's deep industry connections and Scandinavian presence become a genuine differentiator.

The company's network within European mining gives it access to investment opportunities that everyday investors could never reach on their own, and through Svea Mining, that access becomes available to ordinary shareholders.

A public market vehicle suddenly opens the door to exposure normally reserved for private equity, institutional capital, and government-aligned investors, giving everyday investors a rare entry point into some of Europe's most unique and otherwise inaccessible shareholdings

This approach means Svea will not be confined to its own exploration activities but can build shareholder value through investments in the mineral supply chain where Europe's import dependence is most acute and the upside most compelling.

For investors, a position in Svea Mining offers more than exposure to an exploration mining company. It could provide indirect access to a curated portfolio of European mining assets across multiple commodities and jurisdictions, positioning shareholders to benefit from the generational tailwind of European resource independence.

The case for Svea Mining's properties is best understood through the lens of what has actually come out of the ground around them.

The original Boliden mine, located approximately 30 kilometres northwest of Skellefteå, produced 8.3 million tonnes of ore, yielding 128 tonnes of gold, 411 tonnes of silver, and 118,000 tonnes of copper, an extraordinary haul that made it, for a time, Europe's largest and richest gold mine.

The deposit was never a single-metal story; from the outset, the ore body was defined by copper alongside substantial silver, the same polymetallic signature that has defined the district ever since.

That signature has persisted into the modern era. At the Boliden Area's current operations, ore is processed at grades of approximately 1.5% copper, 6.1% zinc, and 78 grams per tonne of silver, alongside gold, demonstrating that the copper-silver association in this district is not a historical curiosity but an active, ongoing feature of the ore being mined today.

Across the wider Skellefteå field, nearly 30 mines have been brought into production since the 1920s, each tapping into the same volcanogenic massive sulphide system, a geological setting defined by copper, zinc, lead, gold, and silver occurring together within Precambrian volcanic rocks.

Svea Mining's Kalvträsk and Stöverfors permits sit within and on the margin of this exact geological belt, the same VMS system that has reliably hosted copper-silver mineralisation across the district for a century.

While Svea's own properties have not yet been subject to modern exploration, and historical work to date has focused on gold-bearing occurrences, the regional pattern is unmistakable: wherever this geological setting has been systematically explored in the Skellefteå district, copper and silver have been found together, often at scale.

That is the potential Svea Mining is now positioned to test, in a district where the geology has already proven, repeatedly and over a century, exactly what it is capable of producing.

.webp)

The Kalvträsk permit covers approximately 7,000 hectares within the Lappvattnet copper-silver metallogenic zone, on the margin of the Skellefteå VMS district. The permit area lies within a recognised corridor of copper, silver the precise battery and electrification metals at the heart of Europe’s critical raw materials strategy.

Some of the world's most significant mining districts share the same copper-silver signature Svea Mining aims to target.

Poland's KGHM operates the Lubin and Rudna mines as classic polymetallic copper-silver deposits, with Rudna alone grading 2.02% copper and 63 g/t silver across 321 million tonnes of ore.

Montana's legendary Butte district built its early fortune on ore averaging 12% copper and 25 oz/tonne silver.

Olympic Dam in Australia, one of the largest polymetallic deposits on earth, produces copper, gold, and silver from a single giant system, while Peru's Antamina and Ontario's Kidd Creek are both copper-zinc-silver systems that have anchored major mining economies for decades.

These are the kinds of world-class copper-silver systems Svea Mining aims to be cut from, exploring within a geological setting that has, time and again, proven capable of hosting exactly this combination of metals at scale.

The Kalvträsk property benefits from northern Sweden's well-developed mining infrastructure, including existing road access, established transportation corridors, low-cost hydroelectric power, and proximity to mineral processing facilities, all of which would significantly reduce the capital requirements of any future production scenario.

The Stöverfors permit covers 452 hectares within the Skellefteå VMS-Au district itself, the same geological system that hosts active mining operations.

The property sits directly within the Skellefteå VMS system, the copper- and silver-bearing volcanogenic massive sulphide setting that has driven base-metal production across the district, and contains mineralised occurrences (ORED05115 and ORED16308) registered with the Swedish Geological Survey (SGU) within structurally favourable host rocks.

SGU classifies the property as a “significant prospect.”

Svea Mining (Spotlight: SVEA | Frankfurt: SVEA) is positioned at the intersection of several powerful tailwinds: a prolific and actively producing copper-silver mining district, a structural global copper-silver deficit, and surging EU demand for domestically sourced critical minerals under the Critical Raw Materials Act.

The conviction on this property is grounded in several compelling fundamentals. It sits within the Skellefteå mining district, one of Europe's most productive metallogenic provinces with over a century of continuous mining history.

The project hosts SGU-registered mineral occurrences, with the property recognised by the survey as a setting of clear prospectivity, situated within the same base-metal-bearing system that has supported commercial mining across the district for generations.

Its position within the Skellefteå volcanogenic massive sulphide belt places it among the copper- and zinc-rich mineralising systems of the Fennoscandian Shield, a geological signature that has underpinned major base-metal discoveries throughout the region.

Svea Mining’s technical programme is led by EurGeol Jyri Meriläinen, a Swedish professional geologist with more than twenty years of experience in mineral exploration and mining operations across Sweden and Finland.

Meriläinen previously served as Senior Mine Geologist at LKAB’s Malmberget mine, one of Europe’s largest underground iron ore operations, where he managed exploration programmes, mineral resource estimation, and geological evaluation. He holds a Master of Science degree in Geology and Mineralogy from the University of Oulu and is a registered European Geologist.

Engineering leadership is provided by P.Eng. Mathieu Gosselin of Gosselin Mining AB, a professional mining engineer with over fifteen years of international experience across underground and open-pit operations in Europe, North America, Africa, and the Middle East. Gosselin holds a Bachelor of Engineering in Mining from McGill University.

The company’s capital markets leadership includes CEO Ken Osborne, a CFA charter holder with deep M&A advisory experience across public and private company transactions with enterprise values exceeding $100 million.

A structural copper deficit, a silver market locked in a six-year supply shortfall, the largest European defence rebuild in generations, and billions in EU funding, all converging on the strongest regulatory environment in Swedish mining history. The convergence of these forces creates a rare window for early-stage positioning in European resource companies like Svea Mining AB.

In a market where copper faces a structural supply crisis, silver is being pulled simultaneously toward AI infrastructure, electrification, and defence applications, and the European Union is deploying unprecedented capital to secure domestic mineral supply chains, Svea Mining offers direct, exchange-traded exposure to copper-silver exploration in one of Europe's most established and productive mining districts, led by experienced professionals, accessible through two of Europe's most important stock exchanges, and operating in a jurisdiction that ranks among the top 10 in the world for mining investment.

Svea Mining AB remains a company we believe investors should be watching closely.

Yours Truly,

Wall Street Investor Report.

For more information, visit sveamining.com

.png)

.avif)

.png)

Compensation and Disclosure Notice

This material is a paid advertisement (paid marketing / promotional material) produced and distributed by Euro Digital Media, 71–75 Shelton Street, Covent Garden, London, United Kingdom, WC2H 9JQ (email: [email protected]) under the brand Wall Street Investor Report via www.wallstinvest.com.

Euro Digital Media has been compensated by Svea Mining AB ("Svea Mining" or the "Issuer") in the amount of $500,000 USD (plus applicable taxes) for the production and distribution of this content. This constitutes a potential conflict of interest.

This information is provided in accordance with applicable rules on marketing communications and transparency under the EU Market Abuse Regulation (MAR).

Euro Digital Media does not hold any shares, options, warrants, or other securities or derivatives of Svea Mining AB at the time of publication, but may purchase or sell such securities in the future without further notice.

This notice is intended to transparently disclose the compensation received and potential conflicts of interest.

ISSUER AND MARKET INFORMATION

Issuer: Svea Mining AB Registered office: Sweden

Stock exchange listings:

The ticker symbols and exchanges listed above are provided for informational purposes only and do not imply any endorsement by the respective exchange.

NATURE OF MATERIAL — ADVERTISEMENT, NOT INDEPENDENT ANALYSIS OR INVESTMENT ADVICE

This document is promotional material and does not constitute independent investment research, an investment recommendation, or investment advice under applicable legislation, including MAR or MiFID II.

This material has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Nothing in this communication constitutes investment advice, financial advice, legal or tax advice, or a solicitation to buy or sell securities. All content is general in nature and has not been tailored to the individual needs of any particular investor.

Nothing in this document should be construed as:

Investors should conduct their own independent assessment and consult their own professional advisers before making any investment decision.

RISKS AND SPECULATIVE INVESTMENT

Investments in exploration and mining companies are highly speculative and involve substantial risks.

Key risks include, but are not limited to:

There is no guarantee of future results. Investors may lose all or part of their invested capital.

FORWARD-LOOKING STATEMENTS

This material may contain forward-looking statements based on current expectations and assumptions. Terms such as "expects," "plans," "intends," "believes," "estimates," "could," "may," "potentially," or similar expressions identify such statements.

Actual results may differ materially from those expressed or implied in forward-looking statements due to various risk factors and uncertainties.

Forward-looking statements do not constitute a guarantee of future developments. Euro Digital Media assumes no obligation to update such statements.

CONFLICTS OF INTEREST

Euro Digital Media received compensation from the Issuer in the amount of $500,000 USD (plus applicable taxes) for the creation and distribution of this communication. This constitutes a material conflict of interest.

No compensation was provided in the form of shares, options, or other securities.

The Issuer or its representatives reviewed factual statements prior to publication and retained editorial control with respect to factual accuracy and final wording.

Employees, contractors, or affiliated parties of Euro Digital Media may currently or in the future hold or trade positions in the securities referenced herein.

HISTORICAL EXPLORATION RESULTS

Historical exploration results, historical sampling, or historical mineralization data have not been independently verified by Euro Digital Media and are not necessarily indicative of future results or economically mineable mineral resources.

NO REGULATORY APPROVAL

This material has not been reviewed, approved, or endorsed by the Swedish Financial Supervisory Authority (Finansinspektionen), BaFin, the Spotlight Stock Market, the Frankfurt Stock Exchange, or any other authority or regulated marketplace.

GERMANY / EUROPEAN UNION (BaFin / MAR)

This communication constitutes a promotional communication within the meaning of Article 20 of the Market Abuse Regulation (MAR) and is not an independent financial analysis report.

It is intended solely for general advertising and informational purposes. Material conflicts of interest and compensation received have been disclosed above.

SWEDEN — SWEDISH MARKETING ACT (MARKNADSFÖRINGSLAGEN 2008:486)

In accordance with the Swedish Marketing Act (Marknadsföringslagen 2008:486), this material is clearly identified as advertising and marketing.

NO OFFER / GEOGRAPHIC RESTRICTIONS

This communication does not constitute an offer or solicitation to buy or sell securities in any jurisdiction where such an offer or solicitation would be unlawful.

Recipients of this communication are solely responsible for complying with local laws and regulatory restrictions.

THIRD-PARTY TRADEMARKS AND RIGHTS

All trademarks, logos, and trade names are the property of their respective owners. The mention of third-party companies or exchanges does not imply endorsement or recommendation.

CONTACT

Euro Digital Media 71–75 Shelton Street Covent Garden London, United Kingdom, WC2H 9JQ Email: [email protected] Website: www.wallstinvest.com

First publication date: 1 July 2026 Channel: www.wallstinvest.com (Wall Street Investor Report)

© 2026 Euro Digital Media. All rights reserved.